This is part of why it's important to attend to one's own financial security -- if one doesn't have a safety fund (6 months of living expenses minimum) that should be number one priority. makes all the difference when navigating employment transitions.

I also really liked the suggestion elsewhere in the comments to negotiate in the offer letter/contract 3 months of pay after the last day of work. I haven't tried that but it's something I'll consider in the future.

The 'six months of living expenses minimum' plus 'fridge+car+laundry machine' fund get touted around a lot, but they ignore the reality that, while living expenses have only been going up, pay has stagnated. Most families are barely scraping by with only ~€300 a month leeway. Assuming €3000 living expenses a month and a combined income of ~€3500 (removing ~€200 a month for random expenses that always pop up), saving €18.000 would take 5 years assuming absolutely nothing bad happens in the mean time. Add to that the fridge+car+laundry fund and some bad luck, and you're looking at 8-10 years of no-fun-expenses-allowed saving. As one would say: get real.

I 50% agree with this, and 50% can't help notice (in the US) restaurants are full, it is common to have a recent iPhone, and 85% of vehicles on the roads are newish SUVs.

Many people are scraping by on minimal income and have minimal expenses.

Many others are scraping by because their spending is out of whack with income.

Of course, reining in spending doesn't address the societal stagnant income problem. It only helps an individual not find themselves in a desperate situation because of job loss.

>> and 85% of vehicles on the roads are newish SUVs.

Average age of vehicles on road hits 11.6 years in the United State, which is a new record. When you have low/under-employment people aren't rushing out to buy new vehicles as they were in the past.

My phone contract costs me 25 pounds a month for an iPhone 6s (new at the time). With an older iPhone, that would have been closer to 15 a month. (Which incidentally is the sim only price of the plan I'm on).

Regarding vehicles. There's almost certainly a bias there. I'm on foot at the moment, and looking at the main road in front of me, the majority of the vehicles are 6-8 years old small to medium care, with a more modern saloon being more common than an SUV.

However many people rely on cars, and unless you're clued in it's easy to overbuy. If my car broke down today and i needdd it to get to work, my options are (broadly) buy an 800 pound banger, buy a 3-5k 5-6 year old vehicle or buy a new vehicle. If I have. O money, then buying an 800 pound banger isn't an option. I don't know where I'd go to get a loan for less than a thousand pounds, other than a payday loan company, or possibly a credit card. Meanwhile, I can walk into my bank ask for 5000 pounds for a car loan and leave with the cash in my account, with no deposit, no security. Funnily enough when you look at the repayments of one of those loans, they come out at near identical to a PCP (or PCH, not sure which) lease agreement on a brand new car, probably a model or two better than the one I could buy with a loan.

Recent iPhones are cheap. You get them with the contract. And for most carriers, choosing not to get the subsidized phone doesn't affect the monthly cost of service.

You'll need a citation for the 85% of vehicles are newish SUVs stat.

Not many. And in the US, if you choose not to take the subsidy on your plan, you don't get a lower price. You can switch carriers, but a lot of those discount carriers suck. So if you're going to be charged for the subsidy anyway, best to get the best phone you can, if for nothing but future proofing.

Yet many of those same families don't bat an eye when taking out loans for nicer cars than they actually need, maxing out the amount of mortgage they can afford, buying the latest TV or game system on credit, etc..

I don't underestimate how hard it is to save, but also many people are perfectly happy buying more than they need to maximize what they can do with their income in the short run..

Also: any family should be saving for retirement, childrens education expenses, etc. anyway.. so long as the first-level pool is liquid enough to support emergencies such as this, it should work as well. Might have to work another year when older, do some sort of side job, or take some other cuts, but point stands

I understand that many people really truly don't have any other options. Their kids need to be fed and clothed, etc. Or maybe they just don't earn much due to the economic landscape or whatever. It can happen easily and quickly, unfortunately. I certainly don't blame these people for not saving!

On the other hand, its because these things can happen so quickly and easily that one should really prioritise getting a little safety net tucked away. I'm not saying "no-fun-expenses-allowed", but putting away something is a good idea (or paying off (some of) the high-interest debts like credit card debt would be a good too), if you can at all afford it.

€3000 a month? Where do you live? Or do you talk about a 4 people family? In a family you also have two incomes, pay less taxes, and actually don't have a 2x increase in costs, since many costs can be shared.

On €1500 you can live quite well in most of Europe. And getting a 6-month safety package shouldn't take more than two years to save up.

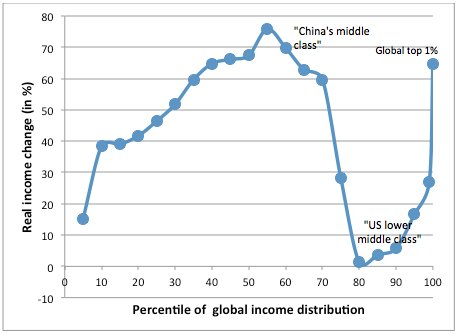

It's a very multi-faceted problem. This[1] graph about the Chinese vs Western middle class is very telling. The world is equalizing due to globalization, and as they say, equality feels like oppression (in this case depression) to the privileged.

There's also the fact that as urbanization continues, real estate in big cities will keep raising in price. People will see real estate more and more as an investment. This completely chokes the housing market since everyone overpays, everyone thinks 'fuck you, I want to get mine', housing becomes unaffordable for starters.

Then there's automation which also hits the middle class a lot. A lot of jobs are cheaper fulfilled by manual labor than automation, and difficult jobs are yet out of the reach of machines.

Add to that the fact that ever more wealth keeps getting stuck at the top (especially the 0.1%) and its a very bad cocktail.

A good beginning to fix it would be an inheritance tax of 100% with a cutoff at ${million} (1 million? 10 million? whatever is reasonable but doesn't give your kids a crazy advantage). Assets would count towards this. Right now we're in a sort of pseudo-feudal system where once you're over a certain amount of wealth, your family/kin is set for life. I'm not against working hard and leaving something for your kids, but there should be limits.

A negative income tax (a sort of basic income light) would also help, as there would always be a proper fallback should you ever have bad luck. It also moves a lot of leverage from employers to employees.

Cities (especially big cities) should no longer seek to extract the maximum amount of tax per piece of ground (resulting in only expensive developments) but should have policies that aim for maximum societal gain: this means building housing to the exact class percentages of the population. 10% rich, 40% middle class and 50% working class in the country? That's what cities should aim for.

Universities should be public and admit students purely on merit. No legacy systems, no positive discrimination. However, I am okay with limiting foreign students (say 10-20% max).

Even with all these things I am probably missing a ton of pitfalls. As I said, its an extremely complex, multi-faceted problem.

"Cities (especially big cities) should no longer seek to extract the maximum amount of tax per piece of ground (resulting in only expensive developments) but should have policies that aim for maximum societal gain: this means building housing to the exact class percentages of the population. 10% rich, 40% middle class and 50% working class in the country? That's what cities should aim for."

This. Unfortunately it's fallen out of fashion... everyone wants to become the richest city in the world, even if all it means is that you will price yourself out of it, literally delivering it in the hands of the few 0.1% for whom it's just another new toy to play...

{kind=link}

This is part of why it's important to attend to one's own financial security -- if one doesn't have a safety fund (6 months of living expenses minimum) that should be number one priority. makes all the difference when navigating employment transitions.

I also really liked the suggestion elsewhere in the comments to negotiate in the offer letter/contract 3 months of pay after the last day of work. I haven't tried that but it's something I'll consider in the future.