Someone walking away from a house doesn’t destroy the house.

The lender’s risk is therefore limited to the difference between purchase price and actual value of the property. Which is something they can hedge or simply not make a loan if they think the property is wildly overvalued.

>Someone walking away from a house doesn’t destroy the house.

The experience of the foreclosure crisis seems to differ. I know people who moved into houses where holes were punched into walls and everything was removed that could be, from door knobs to outdoor deck planks.

You describe damage to a property that a bank owns. Therefore the costs fall on the bank. This is part of the definition of the concept of "taking on risk" and if banks are not accounting for these outcomes in their business model, they're simply bad at business.

This is only true for a federally backed mortgage. Yes, down payment levels, in the context of whether someone needs mortgage insurance, is set by regulation. But down payments can be much less significant if you’re ok with mortgage insurance. Down payments required by banks were typically higher before regulation.

Before regulation it really depended on the buyer. Some people where putting down 5% without insurance, others had much stricter requirements.

We’ve settled on a really arbitrary system where for example the Federal Housing Administration requires huge upfront FHA insurance payments without regard for down payment size if it’s less than 20%. If you’ve saved up say a 8% down payment you really should be a significantly lower risk than someone putting down 3.5%.

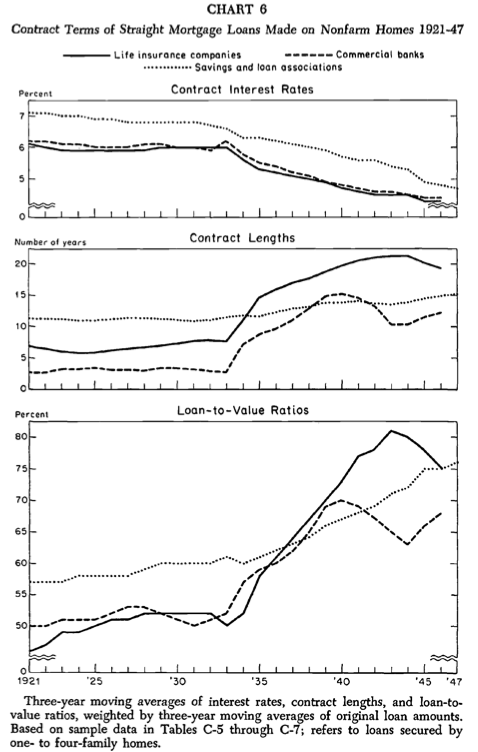

The buyer wasnt the decider. The bank was because they were the one taking the risk. The down payment required by banks before regulation was often 30% or more. That’s partly why home ownership was much lower prior to WW2.

I suspect we’re looking at this through different temporal lenses. When I talk about regulation, I mean the last 100 years in its entirety, not just since the financial crisis of 2008. I agree with some of your point regarding how thresholds are set arbitrarily, though.

> The down payment required by banks before regulation was often 30% or more.

I am talking about lending before regulation. High down payments were not universally applied, so yes sometimes a loan might require 40% but other borrowers might offer nothing. My point is you can’t simply say the required amounts were excessively high some of the time because they weren’t universal and selected based on a perception of risk.

Yes (except in the cases of short sales, where I’ve seen the same). My point was not about who assumes that risk, just pushing back on the idea that people wouldn’t damage a house they were going to be forced out of.

A down payment of 20% provides some of that exact cushion (and makes it less likely for a borrower to casually walk away from a house that fell in value or was otherwise a poor purchase).

Any regard is a really low standard, minimal is more accurate. You don’t end up with nice round numbers like 20% which never changes due to economic conditions etc from calculating some formula.

The global range is wider than that and reflects the reasonable range of this kind of regulation. If it’s say 75% then what’s the point of a loan? On the other hand if it’s 1% what’s the point of the regulation?

Regulators are basically picking a number between 3.5% to 35% and 20% is a nice round number in the middle of that range.

{kind=link}

The lender’s risk is therefore limited to the difference between purchase price and actual value of the property. Which is something they can hedge or simply not make a loan if they think the property is wildly overvalued.